Riyadh - EcoPulse24 | Investigative Report

On an autumn morning in 2018, a young Saudi man sat in his bedroom in Riyadh, his fingers moving at lightning speed across a keyboard. He wasn't studying at a prestigious university, nor working at an oil company or investment bank. He was gaming. And by the end of that month, he had earned $120,000 from a single esports tournament. His father, who had spent years watching him "waste his time" in front of a screen, couldn't believe his eyes when his son received a check for that amount. As for the son, he knew one thing with absolute certainty: the world had changed. And gaming was no longer just gaming.

This story isn't a romantic exception in an accelerating digital age. It's merely one of millions of stories that tell how video games transformed from a hobby practiced by children in their bedrooms into a colossal industry with revenues reaching $187.7 billion in 2024, surpassing the combined revenues of the global film and music industries. But numbers alone aren't enough to understand this phenomenon. The real story lies in the deep economic and social transformations this industry has brought about, in the way it has redrawn the map of global economic powers, and in the unprecedented role Gulf states have begun to play in this changing landscape.

The Digital Empire: When Gaming Transcends Entertainment

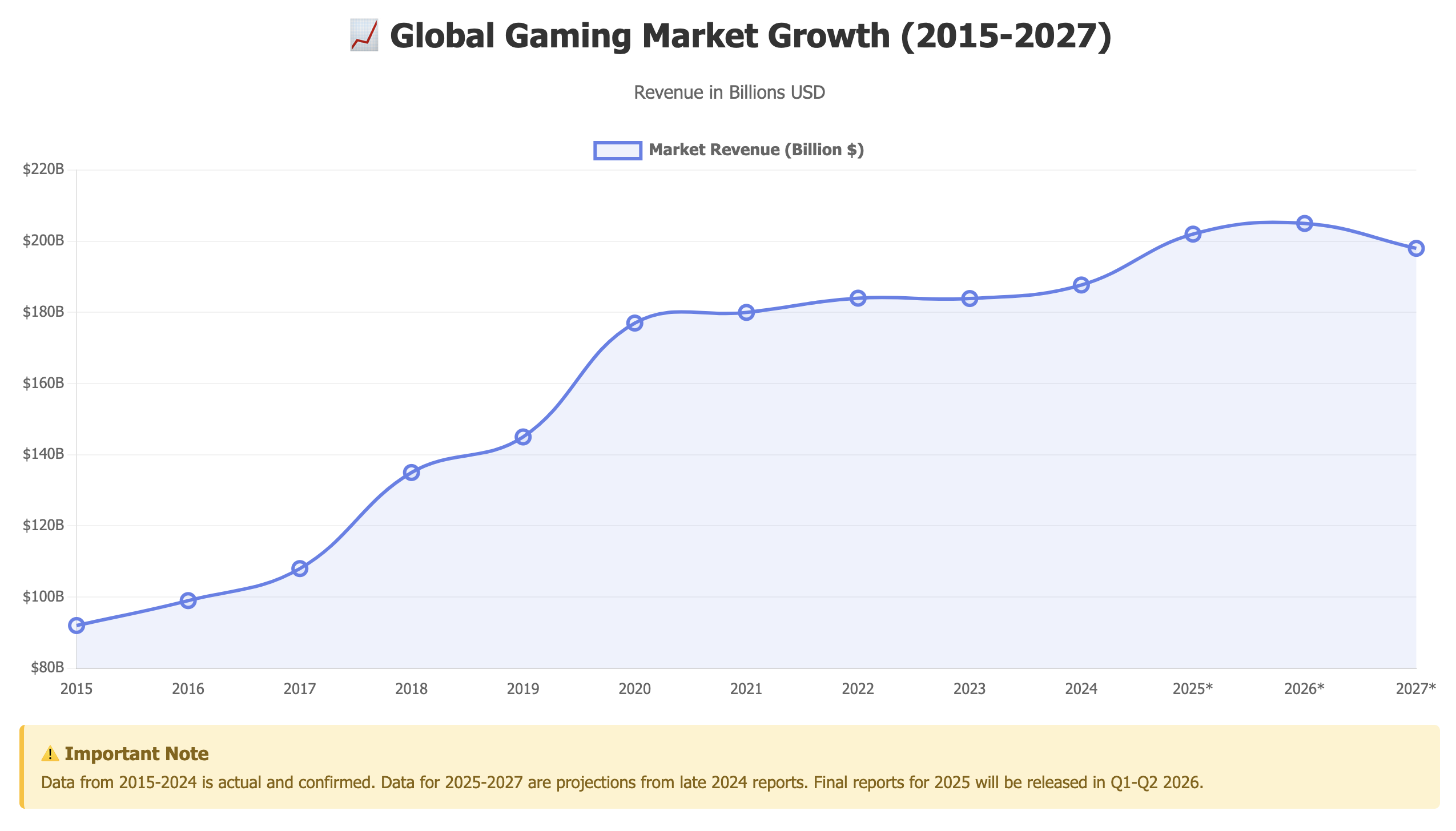

In 2024, the video game industry achieved revenues of $187.7 billion, with annual growth of 2.1% compared to the previous year. This massive figure places the industry above the global film industry, which generated $100 billion, and the music industry, which reached $26 billion in revenues. But what makes these numbers even more interesting is the trajectory the industry has taken over the past decade.

In 2015, the industry was generating $92 billion annually. Then came the COVID-19 pandemic in 2020, creating a quantum leap as revenues jumped to $177 billion with billions of people staying home searching for ways to entertain themselves and socially connect. After the pandemic ended, growth slowed slightly to settle at $183.9 billion in 2023, then $187.7 billion in 2024. Forecasts indicate the industry might reach $200-205 billion in 2025, but these are merely projections based on reports issued at the end of 2024, and actual figures won't be available until Q1 2026 when major companies release their annual financial reports.

What distinguishes this growth is the radical transformation in how games are consumed. In 2024, digital sales reached 95% of total sales, while physical copies declined to just 5%. On the PlayStation platform, one of the world's largest gaming platforms, physical sales didn't exceed 3% of total revenues. This complete digital transformation wasn't merely a change in distribution method, but a complete restructuring of business models and revenues in the industry.

The Economic Geography of Gaming: When the Map Determines Who Wins

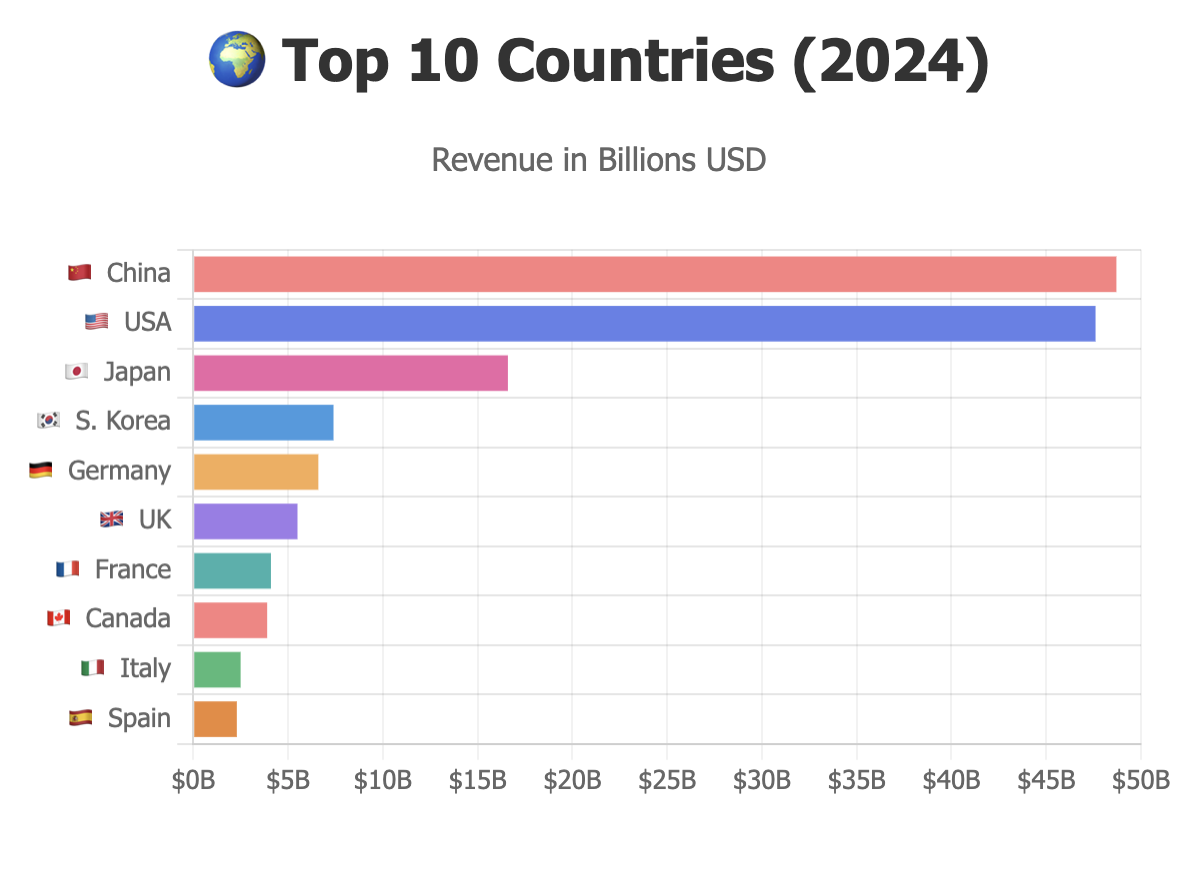

To deeply understand the industry, we must look at its geographical distribution. The shocking truth is that just ten countries control 79.5% of global industry revenues. China tops the list with revenues of $48.7 billion, representing 26.6% of the global market, followed directly by the United States with $47.6 billion or 26% of the market. Together, these two countries capture 53% of total global industry revenues.

Japan ranks third with $16.6 billion, despite a notable decline of 7% in 2024. But this decline doesn't mean weakness in the Japanese market; rather, it reflects the nature of major game release cycles. Japan remains home to industry giants like Nintendo, Sony, Capcom, and Square Enix, and still possesses a deep gaming culture dating back to the 1980s. The average per capita spending in Japan is $238 annually on games, among the highest rates globally.

South Korea comes fourth with $7.4 billion, a global leader in esports where gaming has become a national sport followed by millions of Koreans. Germany fifth with $6.6 billion as the largest European market, followed by the United Kingdom with $5.5 billion, France with $4.1 billion, Canada with $3.9 billion, Italy with $2.5 billion, and finally Spain with $2.3 billion.

Regional distribution reveals clear dominance by the Asia-Pacific region, which captures 46% of the global market, followed by North America with 23%, then Europe with 21%, and finally the rest of the world with 10%. But emerging markets are experiencing stunning growth rates. Turkey is growing at 28% annually thanks to smartphone proliferation, Mexico at 21% with improving internet infrastructure, and India at 17% driven by 600 million youth under 35. India specifically deserves attention, as mobile gaming represents 90% of its gaming revenues, and it may enter the list of the world's top ten markets within the next three to five years.

China: From Ban to Dominance

China's story with video games deserves its own chapter. In 2000, the Chinese government banned video game consoles under the pretext of "protecting children from harmful content." But this ban didn't stop Chinese people from gaming; it pushed them to shift to mobile and computer games. A small company called Tencent was watching this shift intelligently.

In 2011, Tencent acquired the American company Riot Games, maker of League of Legends, for $400 million. Everyone thought it was an insane deal. Today, League of Legends alone generates $2 billion annually, and Tencent has become the world's second-largest gaming company with revenues of $27.7 billion in 2024. The company didn't stop there; it acquired 84% of Finland's Supercell, 40% of America's Epic Games, and invested in Ubisoft, Activision Blizzard, and dozens of other companies. China, which banned games, now controls a large portion of the global industry.

But this dominance comes at a price. The Chinese government still imposes strict restrictions on the industry. In 2021, it limited minors' gaming time to just three hours weekly, and in 2024 proposed banning paid "loot boxes," causing Tencent's stock to crash 10.3% in a single day. The government temporarily backed down from the proposal, but the message was clear: even the world's largest gaming companies are subject to political whims.

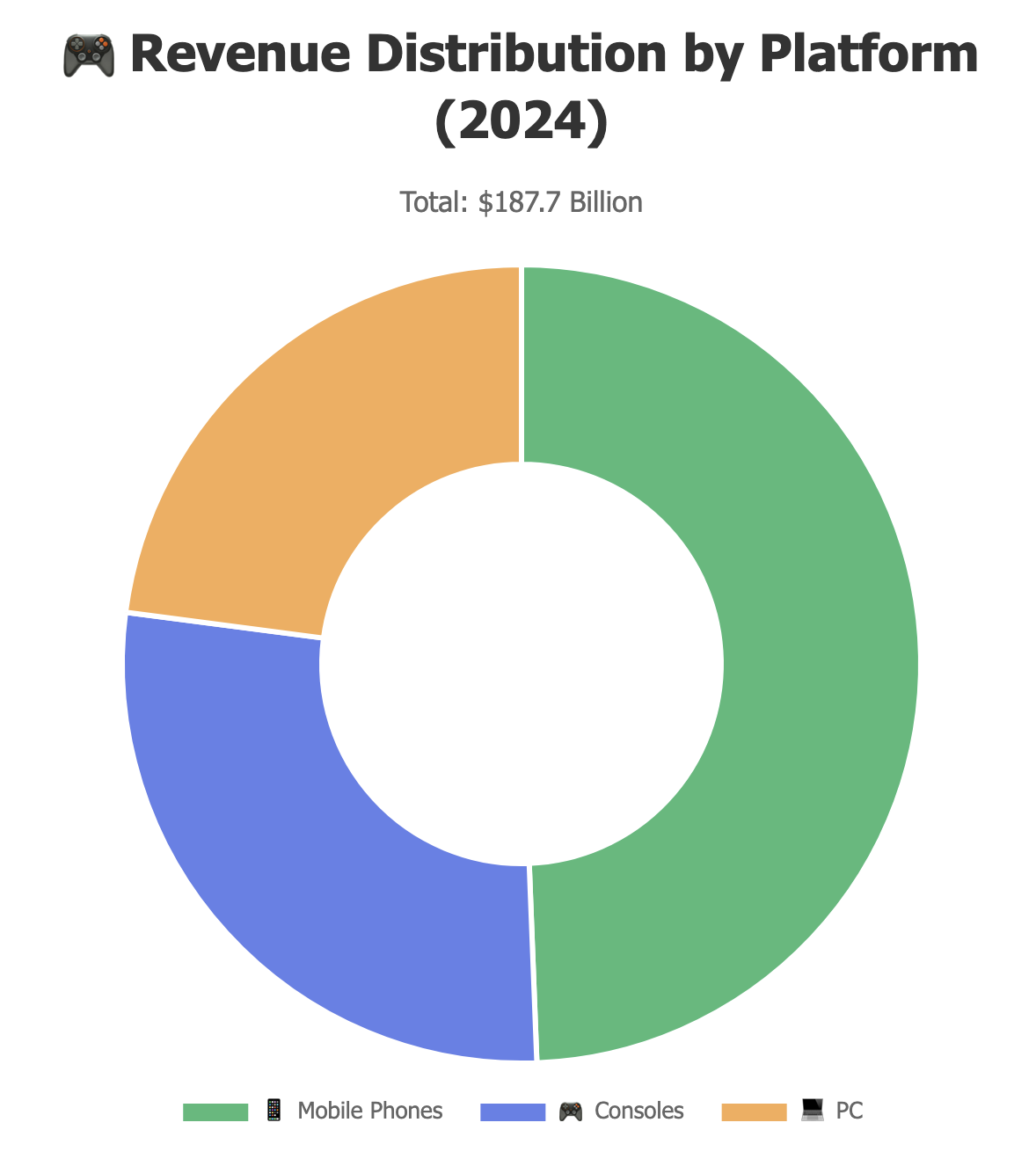

The Three Platforms: Where the World Divides $188 Billion

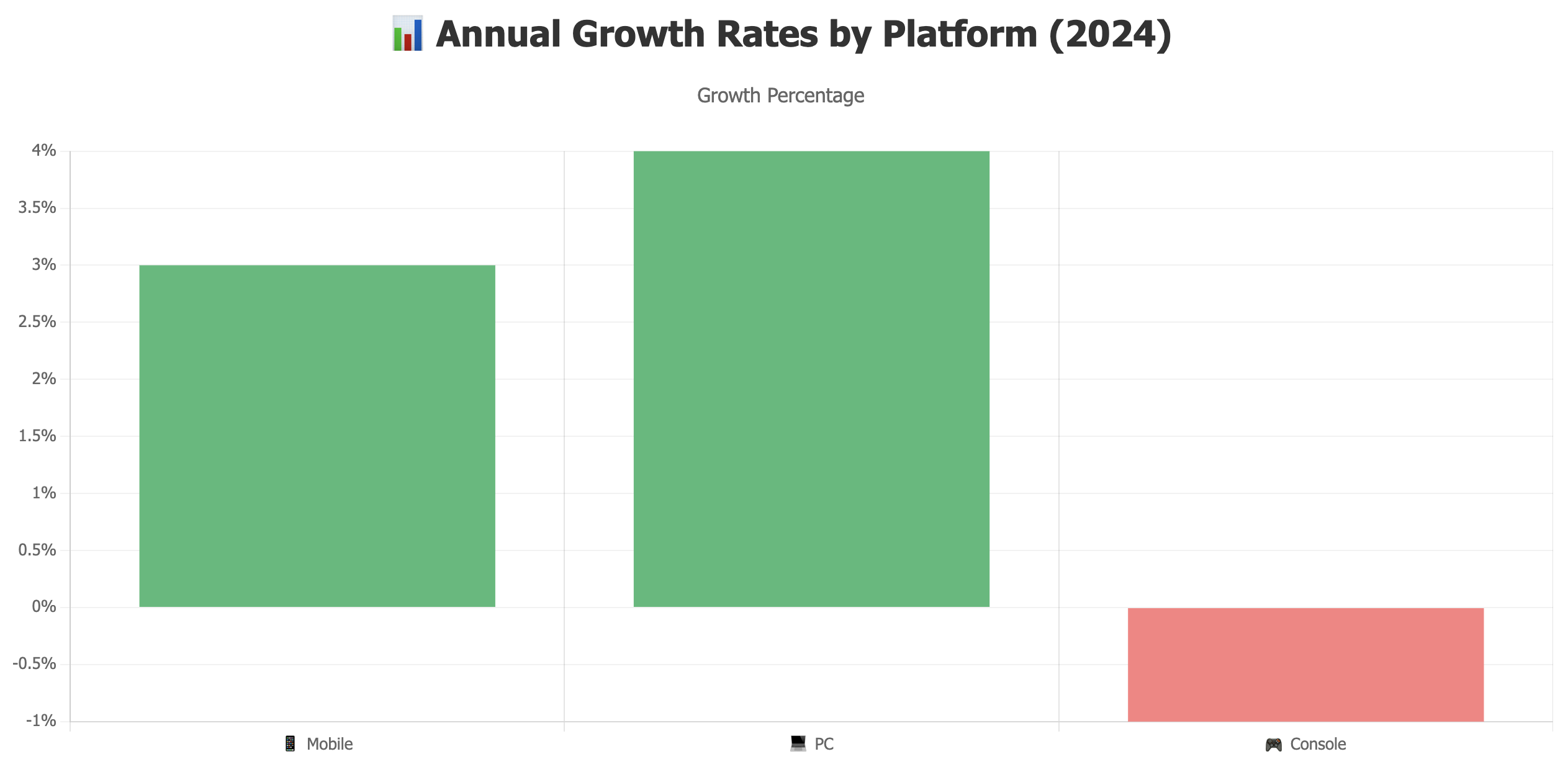

Revenue distribution by platform reveals a shocking reality for many. Mobile phones clearly dominate the industry, generating $92.6 billion in 2024, representing 49% of the total market, with annual growth of 3%. The reason is simple: there are 3.3 billion people gaming on their phones, equivalent to 42% of the world's population. The phone is in every pocket, its games are generally free, and the revenue model relies on advertising and small in-game purchases that seem innocent but generate billions of dollars.

Console devices (PlayStation, Xbox, Nintendo) generated $51.9 billion, representing 28% of the market. But this sector witnessed a slight decline of 1% in 2024 due to the scarcity of major exclusive games. Forecasts indicate growth will return in 2025 with the launch of Nintendo Switch 2 and new exclusive games for PlayStation and Xbox.

Personal computers generated $43 billion, or 23% of the market, with healthy growth of 4%. This growth is primarily driven by the Steam platform, which surpassed 40 million concurrent users for the first time in 2025, achieving the highest revenues in its history.

The Digital Empires: Who Rules the Billion-Dollar Industry?

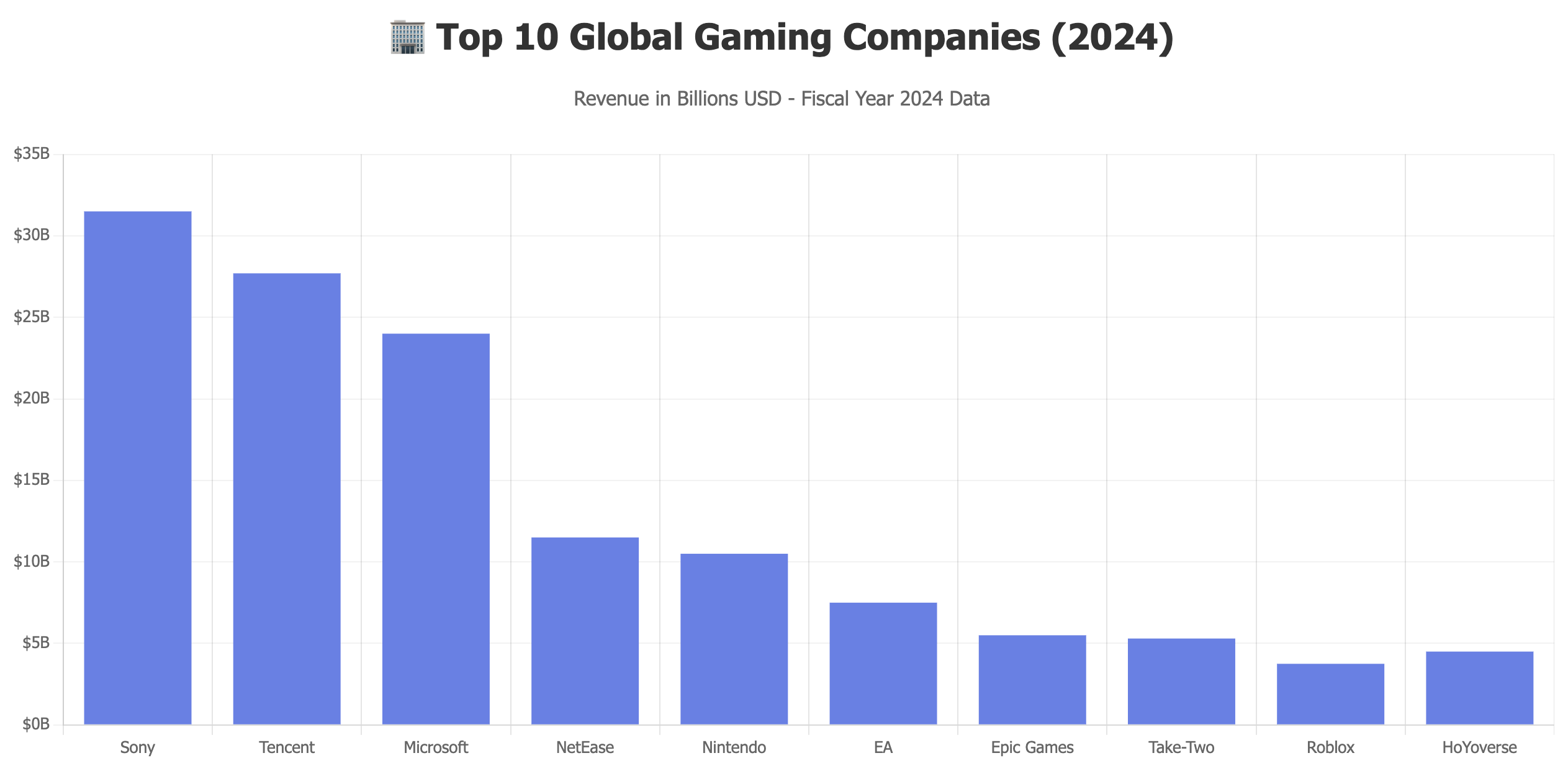

Sony Interactive Entertainment tops the list of the world's largest gaming companies with revenues of $31.5 billion for the fiscal year ending March 2024. PlayStation 5 sold 65.5 million units through Q2 2024, and PlayStation Plus service witnessed 20% revenue growth. But more important than that is the digital transformation Sony experienced, as digital sales came to represent 70% of total software sales, while physical sales declined to just 3%, the lowest figure in the company's history. This transformation made Sony focus on average revenue per user (ARPU) instead of sales volume, and on subscription services and long-term games.

Tencent comes second with revenues of $27.7 billion from the gaming sector alone, distributed between $19.6 billion from the Chinese market with 10% growth, and $8.1 billion from international markets with 9% growth. The company owns a massive portfolio of successful games, from Honor of Kings which generated $1.87 billion in 2024, to PUBG Mobile with $1.15 billion. But more important than that is its strategic investments in global companies, and its massive investment in artificial intelligence where it tripled its capital expenditure in 2024 to reach 76.8 billion yuan, while doubling AI-powered cloud revenues.

Microsoft holds third place with revenues ranging between $23-25 billion, but its strategy is completely different. After acquiring Activision Blizzard for $68.7 billion in 2023, the largest deal in gaming history, Microsoft realized the industry's future isn't in selling devices but in services. Xbox Game Pass with 34 million subscribers paying monthly subscriptions for access to hundreds of games, and Cloud Gaming service allowing play on any device, have become the company's strategic focus. The result: Xbox device sales declined 29% in 2024, but Microsoft doesn't care because it earns more from services and content.

Nintendo fourth with revenues ranging between $10-11 billion, maintaining its unique strategy of focusing on exclusive family games and not entering the technical specifications race. Switch sold more than 146 million units since launch, but sales slowed in 2024 as the device's lifecycle nears its end. Forecasts indicate Switch 2 will launch in 2025, which may reignite growth.

NetEase of China fifth with revenues of $11-12 billion, representing the growing Chinese challenge to Western companies. Its game Marvel Rivals launched in December 2024 reached 20 million players in just two weeks, and estimates indicate it will generate $1 billion in its first year.

Electronic Arts sixth with $7.4-7.6 billion, relying primarily on its sports game series, especially EA Sports FC (formerly known as FIFA) and the Ultimate Team model based on in-game purchases. Epic Games seventh with $5-6 billion, generating most revenues from Fortnite and from the Unreal Engine used by most game developers globally. Take-Two eighth with $5.3 billion, relying on the Grand Theft Auto series which has generated over $2 billion since launch. Roblox ninth with $3.7-3.8 billion, a unique platform where players themselves create content within a complete digital economy comprising over 70 million daily users. And finally HoYoverse tenth with estimated revenues ranging between $4-5 billion, generating most from the Genshin Impact game that has become a global phenomenon.

Revenue Models: How the Free Game Became a Gold Mine

The biggest transformation in the industry wasn't in technology but in business models. In the 1990s, you'd buy a game for forty dollars, play it until finished, then look for another game. This simple model completely collapsed with the internet's emergence.

World of Warcraft in 2004 was the first shock. It didn't sell the game once, but imposed a monthly subscription of $15. Everyone objected: "Who will pay $180 annually to play?" The answer was 12 million people, generating over $1 billion annually for a single game. The economic model broke for the first time.

Then came the smartphone in 2007 to reinvent the industry again. Angry Birds in 2009 was a completely free game, generating revenues from selling small additional items for 99 cents. People mocked the idea. In 2011, the game generated $200 million. A company of 12 employees competing with cinema giants. The model broke a second time.

Clash of Clans in 2012 took the idea to a new level. A completely free game, but if you want to build faster, pay; if you want a stronger army, pay; if you want cosmetic features, pay. Everyone thought: "No one will pay." Reality was completely different. Clash of Clans has generated $10 billion since launch, and some players spent over $1 million on a single game. In 2016, Tencent bought the developer Supercell for $8.6 billion.

Today, revenue models in the industry vary between in-game purchases generating tens of billions annually, the Free-to-Play model where the game is free and income comes from internal purchases (Fortnite is a perfect model generating billions annually without selling the game at all), subscriptions like Xbox Game Pass with 34 million subscribers and PlayStation Plus whose revenues grew 20% in 2024, and in-game advertising which grew 40% in 2024 thanks to high targeting accuracy.

Esports: From Bedrooms to Global Stadiums

In July 2019, Arthur Ashe Stadium, which hosts the US Open tennis finals, was used for the Fortnite World Cup. 23,000 spectators in the stadium, 2.3 million viewers online, total prizes $30 million. The winner was a 16-year-old child named Kyle Giersdorf, who received $3 million, more than the Wimbledon tennis prize.

This scene summarizes the transformation that occurred in esports. In 2024, the esports market reached $3.8 billion with 4.6% growth over 2023, and forecasts indicate it will reach $10.1 billion by 2033 with an annual growth rate of 17%. The revenue model varies between advertising and sponsorships from tech companies, automakers, and energy drinks; live streaming rights on platforms like Twitch and YouTube Gaming; and tournament tickets generating millions of dollars per event.

The League of Legends World Championship in 2024 was watched by over 100 million people worldwide. The International for Dota 2 offered prizes exceeding $40 million. Professional players earn millions of dollars annually from tournaments, live streaming, and sponsorships. The Saudi story of Mosaad Al-Dossary summarizes this transformation: a young man from Jeddah started playing FIFA at twelve, his father a doctor wanted him to continue in medicine, but Mosaad won the FIFA eWorld Cup twice consecutively in 2017 and 2018, earning $500,000 from prizes alone, not to mention contracts and sponsorships. Today, Mosaad is a world champion earning more than most doctors, and his father has become his biggest supporter.

Gulf States Redraw the Map: Strategic Investments Worth Tens of Billions

In February 2022, something unprecedented happened in global gaming industry history. Saudi Arabia's Public Investment Fund announced investments worth $38 billion in the video game sector. This wasn't merely a financial investment, but a clear declaration of Saudi Arabia's intention to become a major player in the industry of the future.

The Saudi strategy wasn't naive. Instead of trying to "make Saudi games" from scratch, which might take decades and cost billions without guaranteed success, Saudi Arabia chose to invest in the industry's global best. Savvy Games Group, the Public Investment Fund's investment arm in the gaming sector, acquired ESL FACEIT Group, the world's largest esports tournament organizer, for $1.5 billion. Then it invested in giant company stocks: 5% of Japan's Nintendo, 5% of Capcom, 9.98% of Korea's Nexon, 8.1% of Sweden's Embracer Group, plus minority investments in Electronic Arts and other companies.

But financial investments were just part of the strategy. Infrastructure was the second part. Qiddiya City, the massive entertainment project near Riyadh, includes advanced centers for esports and spaces for global tournaments. In July-August 2024, Riyadh hosted the Esports World Cup, the largest esports event in history with total prizes of $60 million distributed across 21 different games. The message was clear: Riyadh wants to become the global esports capital.

The strategic goal within Vision 2030 is ambitious but achievable if the current trajectory continues: creating 250,000 jobs in the gaming and esports sector, and contributing 50 billion riyals to GDP by 2030. Building local development studios, attracting global talent, developing Saudi cadres, all part of an integrated plan to transform the Kingdom into a global industry hub.

The UAE chose a different but complementary strategy. Dubai positioned itself as a tech hub connecting East and West, leveraging its world-class infrastructure and business-friendly environment. Dubai Internet City became home to regional offices for global companies like Ubisoft, EA, and Activision. Hub71 in Abu Dhabi works as an incubator for gaming and tech startups. The Middle East Games Summit held annually in Dubai has become one of the region's most important conferences where decision-makers, investors, and developers meet.

The Emirati strategy focuses on attracting companies and talent through tax exemptions, advanced infrastructure, and a strategic location allowing access to 500 million Arabic speakers in the region. Results are beginning to show with local development studios opening and supporting Arabic digital content creation.

Qatar chose to leverage its expertise in organizing major events. After successfully hosting the 2022 World Cup, Qatar realized organizing major events is its core strength. It hosted League of Legends and Valorant tournaments, developed partnerships with Riot Games and Valve, and invested in live streaming infrastructure. Aspire Zone in Doha transformed into an innovation center for sports including esports. The result was an active local market and attracting global sponsorships from companies like Coca-Cola and Red Bull.

Kuwait focused on content creation and live streaming, where Kuwaiti content creators with millions of followers emerged on platforms like Twitch and YouTube, generating revenues from advertising and sponsorships and becoming part of the local digital economy.

Governance and Regulations: When Governments Intervene

With the industry's growth and increasing impact on society and economy, governments worldwide began imposing stricter regulatory frameworks. These laws vary between protecting intellectual property rights and combating piracy, content controls through age ratings for games and banning inappropriate violent or sexual content, esports regulation via tournament licenses and combating manipulation and doping, and finally consumer protection, especially minors from excessive spending.

China represents the strictest regulatory model. Restrictions on minors' gaming time limit it to just three hours weekly, and new game licenses are limited to only hundreds annually from thousands of applications. In 2024, the government proposed banning paid "loot boxes," causing immediate collapse in Chinese gaming company stocks before the government temporarily backed down from the proposal.

Europe focuses on privacy and data protection through GDPR laws imposing strict restrictions on data collection, and special laws on loot boxes where some countries like Belgium and the Netherlands consider them a form of illegal gambling.

In the Gulf, regulatory bodies began forming. Saudi Arabia established the General Authority for Audiovisual Media and the Saudi Esports Federation to regulate the sector. The UAE has the National Cybersecurity Authority and a specialized department in Dubai Sports Council for esports. These legal frameworks aim to protect companies and players alike, increase market credibility, and attract global investments by providing a clear and stable legal environment.

Major Challenges: The Dark Side of the Empire

2024 will be remembered in industry history as the year of record layoffs. 16,766 employees were laid off from gaming companies worldwide, the highest number in industry history, exceeding what happened in 2022 and 2023 combined. Microsoft laid off 1,900 employees after acquiring Activision Blizzard, Sony laid off 900 employees, Unity laid off 25% of its workforce, Epic Games laid off 16% of its employees.

The reasons are multiple but interconnected. First, post-pandemic inflation where companies hired heavily in 2020-2021 thinking exceptional growth would continue, but after life returned to normal, growth slowed and companies became burdened with surplus employees. Second, failure of massive-budget games like Sony's Concord which closed after just two weeks from launch with losses estimated at $200 million, and Warner Bros' Suicide Squad: Kill the Justice League which failed miserably despite its massive budget. Third, the rise of artificial intelligence which companies began using in development and graphics, reducing their need for employees in some departments.

The second challenge is market saturation. 60% of global gaming time is concentrated in just 19 games, most of them old releases like Fortnite, League of Legends, Roblox, and Minecraft. These "evergreen" games dominate the market because players have invested years of time and money in them and built friendships and communities, making the transition to new games psychologically and financially costly. In 2023, thousands of new games were launched, but only five games managed to exceed the threshold of 0.1% of total global gaming time.

Piracy and cybersecurity represent a constant challenge. Game piracy costs the industry billions of dollars annually, and account hacking, virtual currency theft, and attacks on game servers are all ongoing threats. Companies invest heavily in protection technologies like Denuvo, two-factor authentication, and cloud gaming services that are difficult to pirate.

Declining external investments was noticeable in 2024, with venture capital heading to the industry dropping 40%. Investors became more cautious, preferring profitable companies over those focusing on rapid growth, especially amid rising interest rates and high risks.

The Future: Three Possible Scenarios

The first scenario centers on artificial intelligence reinventing everything. Tencent tripled its AI investment in 2024, and other companies are following the same approach. AI will change all aspects of the industry: faster development where games needing five years will be made in one year, better graphics through AI-generated complete worlds, and total customization where each player gets a unique experience designed specifically for them. But the price will be the disappearance of thousands of traditional jobs in development and design.

The second scenario sees the Gulf transforming into a gaming industry superpower. Saudi Arabia and the UAE aren't just investing, but building a complete ecosystem of local development studios, global tournaments, local talent, and attracting global companies. If the current trajectory continues, Saudi Arabia's goal of creating 250,000 jobs and contributing 50 billion riyals to GDP by 2030 seems achievable.

The third scenario predicts complete Chinese dominance. Black Myth: Wukong in 2024 was the beginning, and Marvel Rivals was the confirmation. China has the largest market, largest player base, largest company, lower development costs, and faster innovation. The only obstacle is government restrictions, but if the government eases its grip slightly, China will become the undisputed dominant force.

Conclusion: Not Just Games

When you see a child gaming on their phone in 2025, don't rush to judgment. Perhaps they're learning strategic thinking and teamwork, perhaps training to become a world champion earning millions of dollars, perhaps developing skills that will be essential in tomorrow's job market.

Video games are no longer a children's hobby. They've become a $188 billion industry creating millions of jobs worldwide, a professional sport followed by hundreds of millions, a soft power tool used by nations to extend their influence, and a laboratory for future technologies from artificial intelligence to virtual reality to blockchain.

Saudi Arabia, the UAE, and Qatar didn't enter this industry as spectators. They entered as players wanting to participate in creating the future. The massive investments, advanced infrastructure, global tournaments, all clear signals that the Gulf is betting that the future will be digital.

And thirty years from now, when historians write about the first two decades of the 21st century, they'll discuss the rise of the internet, the smartphone revolution, and artificial intelligence. And they'll discuss video games not as "entertainment," but as an economic and social revolution that changed how we work, communicate, and understand the world. Most importantly, they'll discuss how this revolution proved that play can be the most serious business.

© EcoPulse24 - December 2025