Riyadh | EcoPulse24

From Euphoria to Erosion: The Great Crypto Reckoning

The cryptocurrency market entered 2025 riding a wave of institutional legitimacy and political tailwinds that seemed poised to validate a decade of true believers' predictions. Donald Trump's return to the White House on January 20th marked what many saw as the dawn of a crypto-friendly regulatory era. Two days later, he signed an executive order titled "Strengthening American Leadership in Digital Financial Technology," signaling an administration eager to position America as the global crypto capital.

The fanfare was immediate and substantial. In the first week of January alone, spot Bitcoin exchange-traded funds attracted net inflows exceeding $1.9 billion, with BlackRock's iShares Bitcoin ETF leading the charge at $370.2 million in a single trading session. The total cryptocurrency market capitalization peaked at $3.8 trillion on January 18th, just two days before Trump's inauguration, appearing to confirm that institutional money and political support would finally propel digital assets into the financial mainstream.

But 2025 would become a cautionary tale about the persistent gap between crypto's promise and its performance, between regulatory optimism and operational reality, and between record-breaking peaks and devastating collapses that erased billions in value within hours.

Chapter One: The Rise and Stumble of Institutional Adoption

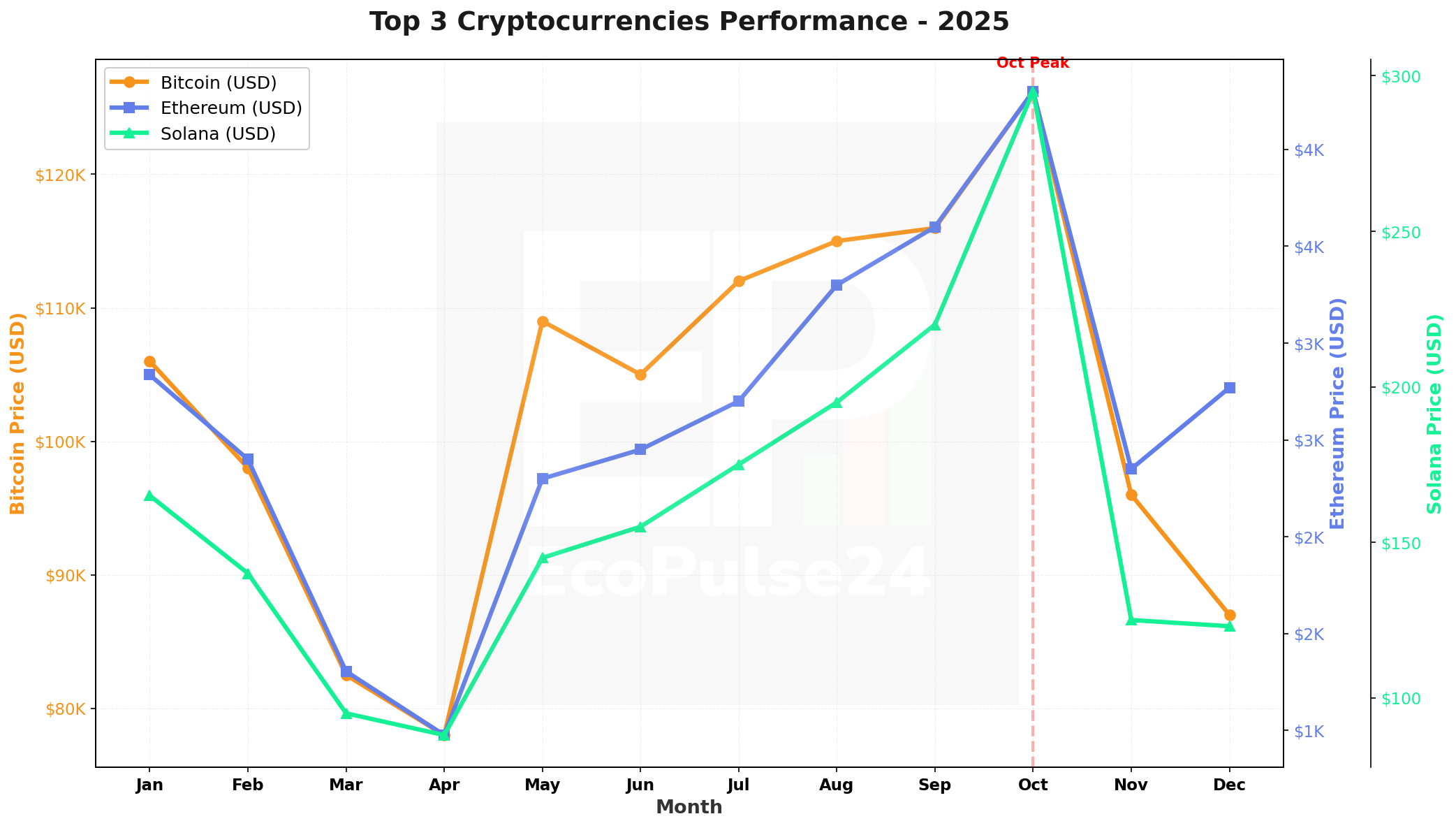

Bitcoin's journey through early 2025 followed a familiar pattern of retail enthusiasm meeting institutional caution. After touching a marginal new all-time high of $106,182 on January 22nd - just two days post-inauguration - the flagship cryptocurrency began a drift that would define much of the year: sideways consolidation punctuated by sharp, violent selloffs.

The establishment of a Strategic Bitcoin Reserve in March generated headlines but little sustained price momentum. The passage of stablecoin legislation through the Senate represented a genuine regulatory milestone, yet markets barely noticed. Even Coinbase's inclusion in the S&P 500 in May, celebrated by advocates as watershed validation, failed to arrest Bitcoin's gradual erosion from its January peak.

Ethereum's struggles proved even more acute. Starting the year at $3,336, ETH began an alarming descent that would see it touch $1,805 by March's end, effectively erasing all gains from 2024. Standard Chartered's March 17th research note crystallized growing skepticism, slashing its year-end price target from $10,000 to $4,000 - a stunning 60% reduction that acknowledged what data had been showing for months: Ethereum was caught in an identity crisis.

The blockchain's Layer 2 scaling solutions, meant to enhance its capabilities, had instead cannibalized its value proposition. Standard Chartered estimated that Coinbase's Base network alone had reduced Ethereum's market capitalization by $50 billion, as transactions migrated to cheaper, faster alternatives built atop the base layer. Meanwhile, Solana captured mindshare among developers building consumer applications, while Bitcoin solidified its narrative as digital gold. Ethereum remained stuck between categories - neither the fastest platform nor the simplest store of value.

Chapter Two: The Bybit Catastrophe - When $1.5 Billion Vanished

If January represented crypto's political coming-out party, February delivered a brutal reminder of its operational immaturity. On February 21st, Dubai-based exchange Bybit suffered the largest cryptocurrency theft in history when hackers drained approximately $1.5 billion in Ethereum from its cold storage wallet.

The sophistication of the attack distinguished it from typical crypto hacks. According to forensic analyses by Chainalysis and blockchain security firms, attackers compromised a developer workstation at Safe{Wallet}, a third-party multisignature platform Bybit relied upon for transaction approvals. By hijacking active AWS session tokens, the perpetrators gained access to Safe's infrastructure without triggering multi-factor authentication.

The attackers then injected malicious JavaScript code specifically designed to activate only when Bybit initiated cold wallet transactions. When company officials approved what appeared on their screens as a routine transfer to a hot wallet, they were actually signing a completely different transaction redirecting 401,347 ETH to attacker-controlled addresses.

Within 48 hours, $160 million of the stolen funds had been laundered through a complex web of decentralized exchanges, cross-chain bridges, and mixing protocols. On February 26th, the FBI formally attributed the attack to North Korean actors under an operation designated "TraderTraitor," urging crypto service providers to block transactions involving identified addresses.

The market impact proved immediate and severe. Bitcoin dropped 20% from its January peak in the days following the breach. Bybit faced a bank run as users rushed to withdraw funds, though CEO Ben Zhou moved quickly to secure bridge loans covering potential unrecoverable losses and publicly confirming other cold wallets remained secure.

Yet the psychological damage extended beyond Bybit's balance sheet. The hack exposed uncomfortable truths about cryptocurrency custody: even sophisticated institutions using industry-standard security practices remained vulnerable to supply chain attacks and social engineering. If a major exchange with professional security teams could lose $1.5 billion, what did that imply about the sector's readiness for mainstream adoption?

Chapter Three: Ethereum's Existential Crisis

While Bitcoin struggled with volatility, Ethereum confronted something more existential: a crisis of purpose and performance. The second quarter saw ETH collapse to $1,476 on April 9th - its lowest level in two years and a staggering 64% below its December 2024 peak of $4,100.

The proximate cause was macroeconomic: President Trump's announcement of escalating tariffs, starting at 10% before climbing to 25% on Chinese and other imports, triggered a risk-off wave across global markets. But Ethereum's decline far exceeded Bitcoin's 23% drawdown over the same period, signaling deeper structural challenges.

The data painted a troubling picture. According to CoinGecko's Q1 2025 report, Ethereum's price fell from $3,336 to $1,805 during the first quarter, wiping out all 2024 gains. Its market capitalization contracted to $178 billion by April, while over $400 million in leveraged ETH positions were forcibly liquidated in a single day. Perhaps most concerning, approximately 40% of all circulating Ethereum was now held at a loss - meaning four in ten holders had purchased at prices higher than current market value.

The ETH/BTC ratio told an even starker story, approaching its historical lows since 2017. Standard Chartered projected the ratio could fall to 0.015 by year-end 2027, representing continued structural underperformance against Bitcoin. Multiple factors drove this decline: Layer 2 networks siphoning transaction fees from the base layer, Solana capturing developer mindshare for consumer applications, and a general lack of clarity about Ethereum's value proposition post-Merge.

Chapter Four: October's Black Friday - When Leverage Met Liquidity

If February's Bybit hack represented an external assault on crypto's infrastructure, October 10th exposed its internal fragility. On that day, more than $19 billion in leveraged positions were liquidated in roughly 24 hours, triggering what became known as "Crypto Black Friday."

Unlike the Terra/Luna collapse or FTX's implosion, this crash stemmed not from fraud but from the toxic interaction of three structural factors: excessive leverage, thin liquidity, and flawed risk management systems.

By early October, open interest in Bitcoin and Ethereum perpetual futures had reached elevated levels, with funding rates climbing from approximately 10% annualized to nearly 30% by October 6th. A significant portion of this exposure sat on venues using unified (cross-asset) margin systems, which work efficiently in calm markets by netting profits and losses across positions. Under stress, however, these systems tie portfolios to their weakest assets.

When Trump announced 100% tariffs on China on October 10th, global markets convulsed. But crypto, operating 24/7 without circuit breakers or trading halts, bore the brunt. As prices fell, margin calls cascaded through the system. Traders forced to sell positions to meet margin requirements pushed prices lower still, triggering more margin calls in a vicious cycle.

The breakdown extended beyond standard liquidations. Several major venues deployed Auto-Deleveraging (ADL) mechanisms - emergency protocols that forcibly close profitable positions to maintain exchange solvency when liquidation engines can't keep pace with losses. Some of the market's best-hedged traders found their positions reduced or eliminated without consent, adding a second layer of risk atop directional exposure.

Total crypto market capitalization vaporized $1.3 trillion in the weeks following October 10th. Ethena's USDe stablecoin, designed to maintain a 1:1 peg with the dollar, traded as low as $0.60 on Binance - a 35% discount indicating complete loss of confidence in synthetic collateral structures. The token saw $8.3 billion in net outflows as users fled to safer assets.

Chapter Five: The Persistent Threat of State-Sponsored Cybercrime

According to blockchain analytics firms Chainalysis and TRM Labs, entities attributed to North Korea stole approximately $2.02 billion in cryptocurrency during 2025, representing a 51% increase over 2024's $1.34 billion. This brought the cumulative total since 2017 to roughly $6.75 billion, according to Chainalysis data.

What distinguished 2025 wasn't just the dollar value but the operational evolution. The number of attacks decreased while their individual scale increased dramatically, suggesting greater sophistication and selectivity in targeting. Beyond the Bybit breach, major incidents included the June hack of Cetus decentralized exchange ($223 million), the July compromise of Balancer protocol ($128 million), and the theft from Phemex exchange ($73 million).

The technical methods evolved beyond traditional email phishing to supply chain attacks, compromising trusted third-party service providers to access primary targets. U.S. and international authorities also documented instances of infiltration by IT workers with fabricated credentials gaining employment at crypto companies to access internal systems and information.

Post-theft, analysis revealed clear patterns in money laundering strategies, including preferences for Chinese-language services, cross-chain bridges, and mixing protocols. The typical laundering cycle extended approximately 45 days following major thefts, with analysts noting that after executing large-scale operations, attack tempo would decrease - suggesting strategic focus on laundering existing proceeds rather than immediately pursuing new targets.

Chapter Six: The Security Crisis Deepens

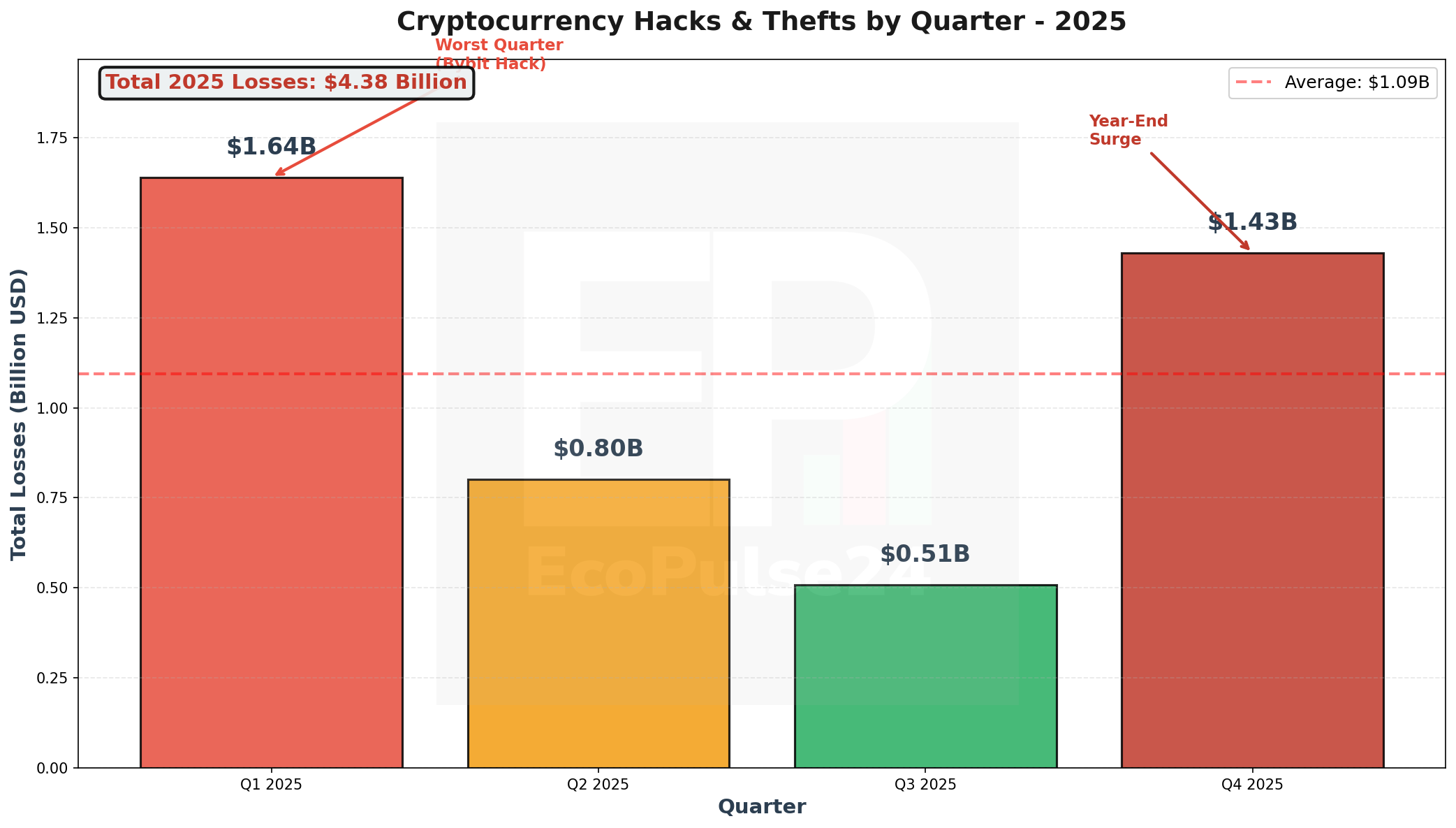

North Korean operations, while the largest single source, represented only a portion of 2025's security failures. Multiple blockchain analytics firms estimated total cryptocurrency thefts between $2.7 billion and $3.4 billion for the year, marking the third consecutive year of record-breaking losses.

The quarterly breakdown revealed troubling patterns. Q1 2025 became the worst quarter on record with $1.64 billion in losses, according to Immunefi. Losses moderated to approximately $801 million in Q2 (down 52%) and $509 million in Q3 (down 37%). However, September saw a record 16 separate million-dollar hacks, indicating continued attacker focus on high-value targets. Q4 rebounded to approximately $1.43 billion, suggesting security improvements remained uneven.

Attack vectors showed clear evolution. In H1 2025, according to CertiK data, wallet compromises accounted for roughly 69% of value stolen - about $1.71 billion across just 34 incidents. Most involved private key theft, seed phrase exposure, or compromised signing devices following malware infections or social engineering. Phishing represented 16.6% of H1 value ($410.7 million) but the highest incident count at 132 cases, making it the leading cause by frequency.

Notably, smart contract vulnerabilities - once the dominant attack vector - contributed only 14.4% of H1 losses. This suggested that code audits and security reviews had improved, but attackers had simply shifted focus to operational weaknesses and human factors.

Chapter Seven: The Price Performance Puzzle

By any traditional market metric, 2025 should have been cryptocurrency's breakthrough year. Spot Bitcoin ETFs attracted $34.1 billion in net inflows, nearly matching 2024's $35 billion. Major financial institutions launched or expanded crypto services. The first comprehensive U.S. stablecoin legislation became law. A crypto-friendly administration occupied the White House.

Yet investors lost money. Bitcoin, despite reaching an all-time high of $126,210 on October 6th, finished the year down approximately 8% from January levels, trading near $87,000 by late December. Ethereum fared worse, declining 10-13% for the year and currently trading around $3,270. Perhaps most telling, approximately 40% of Ethereum's circulating supply sat underwater - purchased at prices above current market value.

The divergence from traditional assets proved stark. While Bitcoin and Ethereum struggled, the S&P 500 gained 19.4% and gold surged 68%. Bitcoin's correlation with technology stocks and gold both broke down during 2025, suggesting the asset class had lost its narrative coherence. Was it a risk asset or a hedge? Did it correlate with tech or function as digital gold? The answer appeared to be neither consistently nor both unpredictably - a problematic position for institutional allocation.

The ETF story contained its own contradictions. While aggregate inflows appeared strong, they concentrated heavily in BlackRock's iShares Bitcoin Trust (IBIT), which alone captured $25.1 billion of the $34.1 billion total. Excluding IBIT, all other spot Bitcoin ETFs combined saw $3.2 billion in net outflows. Grayscale Bitcoin Trust (GBTC) hemorrhaged another $3.7 billion in 2025 atop $21.5 billion lost in 2024.

Ethereum ETFs followed similar patterns. The category attracted $9.9 billion in 2025, but flows concentrated in iShares Ethereum Trust (ETHA) at $9.1 billion, Fidelity Ethereum Fund (FETH) at $1.1 billion, and Grayscale Ethereum Mini Trust (ETH) at $901 million. This extreme concentration suggested not broad institutional adoption but rather specific distribution advantages among dominant players.

More concerning, inflows slowed dramatically in the final months. During the last three months of 2025, crypto ETFs attracted only $790 million total, while several major products experienced outflows amid falling prices. Investors who bought near the peaks suffered significant losses despite selecting regulated investment vehicles - hardly the confidence-building outcome needed for mainstream adoption.

Chapter Eight: Forced Liquidations and Systemic Risk

Beyond hacks and price volatility, 2025 exposed cryptocurrency markets' persistent leverage problem. According to CoinGlass data, approximately $150 billion in notional value was forcibly liquidated throughout the year. While this represented routine margin management in one sense, the concentration and velocity of liquidations during stress periods raised systemic concerns.

The October 10th event alone saw $19 billion liquidated in roughly 24 hours. Additional liquidation waves hit in late December: $600 million on Monday, followed by $400 million each on Wednesday and Thursday. These weren't isolated incidents but symptoms of a market structure that incentivized excessive leverage through high funding rates, then punished it through cascade failures when volatility spiked.

Open interest in Bitcoin and Ethereum perpetual futures fell by a combined $5 billion after October, reducing leverage but leaving markets vulnerable to sharp moves amid thin liquidity. The vulnerability was heightened by year-end options expiries representing over 50% of Deribit's total open interest, creating additional potential for volatility.

Analysts noted a troubling pattern: retail and professional traders alike were using 20-50x leverage routinely, with some venues offering even higher ratios. While this created trading opportunities in stable conditions, it transformed ordinary corrections into liquidation cascades. The October crash demonstrated that crypto's 24/7 trading and lack of circuit breakers meant that once liquidations began, no natural stopping mechanism existed until margin was exhausted or exchanges deployed emergency protocols like ADL.

Chapter Nine: The Altcoin Apocalypse

If 2025 proved challenging for Bitcoin and Ethereum, it proved catastrophic for most alternative cryptocurrencies. The Altcoin Season Index fell to 22/100 by late December - its lowest reading in over 90 days - indicating capital fleeing smaller tokens for perceived safety in Bitcoin.

The data supported this flight to quality. According to CoinGecko's reporting, Bitcoin's market dominance increased 4.6 percentage points during Q1 alone, ending at 59.1% - levels not seen since Q1 2021. By year-end, dominance approached 60%, meaning nearly three-fifths of all cryptocurrency market value sat in a single asset. This represented a dramatic reversal from previous cycles where altcoin rallies typically followed Bitcoin gains.

Several factors drove the altcoin underperformance. First, the sheer proliferation of tokens had saturated the market. With thousands of tradable cryptocurrencies offering marginal differentiation and minimal real-world utility, available capital simply couldn't support such breadth. Second, narratives that had driven previous altcoin seasons - DeFi summer, NFT mania, Layer 1 competitors - had either matured or imploded. Third, institutional money flowing into crypto overwhelmingly chose Bitcoin via regulated ETFs rather than exploring speculative altcoin positions.

Solana exemplified both the promise and peril. After dropping 70% at one point during the year, the blockchain recovered on strength in memecoins and AI agent applications. Yet even this relative success story reflected crypto's continued dependence on speculation rather than utility. The January launch of Trump's TRUMP memecoin on Solana briefly drove activity and helped SOL reach $295 before the inevitable crash.

Major altcoins fared poorly across the board. XRP, despite legal clarity from its SEC settlement, traded down 1.8% in late December. Cardano fell 2.3%, Dogecoin dropped 2.2%, and countless smaller tokens suffered double-digit or worse declines. The few success stories - typically tied to specific narratives or exchange listings - proved fleeting.

Chapter Ten: What 2025 Revealed About Crypto's Future

As the year concluded, several uncomfortable truths had crystallized. First, regulatory clarity and political support, while helpful, couldn't override fundamental issues of security, leverage management, and value proposition. The Trump administration's crypto-friendly stance generated headlines but not sustained price appreciation.

Second, institutional adoption via ETFs, while real, remained highly concentrated and subject to the same volatility that plagued the underlying assets. The notion that "institutional money" would bring stability proved largely illusory when that money entered and exited as rapidly as retail capital.

Third, the security threat from both state-sponsored and criminal actors had grown more sophisticated, not less. Despite industry investment in security infrastructure, major exchanges and protocols continued falling victim to attacks that combined technical exploits with social engineering. The cryptocurrency industry's global, permissionless nature remained both its greatest strength and most persistent vulnerability.

Fourth, leverage and derivatives had evolved into systemic risks rather than mere trading tools. The October crash demonstrated that concentrated leverage positions, unified margin systems, and inadequate liquidity could transform a normal correction into an existential crisis. Traditional finance's hard-won lessons about margin requirements and risk management had been largely ignored, with predictable results.

Finally, the gap between crypto's market performance and traditional assets raised fundamental questions. If Bitcoin and Ethereum couldn't outperform during a year of regulatory clarity, political support, and substantial institutional inflows, when would they? The narrative that crypto represented either a superior store of value or a revolutionary technology platform struggled against the reality of -8% and -13% annual returns while gold surged 68%.

The Path Forward: Lessons and Implications

Yet writing off cryptocurrency based on 2025 alone would be premature. The infrastructure built during the year - regulated ETFs, clearer legal frameworks, institutional custody solutions - represented genuine progress even if prices failed to reflect it immediately. Bitcoin's resilience in maintaining a $1.7 trillion market capitalization despite massive hacks and leverage unwinds suggested staying power, even if spectacular growth proved elusive.

The deleveraging that followed October's crash, while painful, potentially created healthier market structure. Open interest fell more than 40% from October highs. Millions of overleveraged accounts closed. Several major venues tightened leverage limits and improved risk controls. While these changes couldn't prevent future crises, they might reduce their severity.

The security failures, paradoxically, might drive improvements faster than success would have. Each major hack generated forensic analysis, improved monitoring tools, and pressure for better practices. The industry had billions of reasons to solve custody and operational security - motivation that pure price appreciation wouldn't provide.

For investors, 2025 delivered harsh but valuable lessons. Cryptocurrency remained among the most volatile and risky asset classes, where even sophisticated institutions lost billions to hacks and even regulated investment vehicles like ETFs offered no protection against underlying volatility. Leverage amplified gains during rallies but accelerated destruction during crashes. Security assumed paramount importance when billions could disappear through a single compromised workstation.

The year also clarified that cryptocurrency had evolved beyond its cypherpunk origins into a market dominated by the same forces that shaped traditional finance: institutional capital flows, regulatory frameworks, macroeconomic conditions, and professional traders. The romantic notion of a parallel financial system operating outside traditional constraints had collided with the reality that crypto increasingly danced to the same tune as stocks, bonds, and commodities - just with higher volatility and lower liquidity.

Conclusion: A Market at a Crossroads

As 2025 concluded with Bitcoin trading near $87,000 - 31% below its October peak but still elevated versus historical norms - the cryptocurrency market stood at a crossroads. One path led toward further integration with traditional finance: more ETFs, clearer regulations, institutional custody, and eventually, perhaps, genuine utility beyond speculation. This path promised stability and legitimacy but risked diluting the decentralized, permissionless ideals that birthed the sector.

The alternative path led toward renewed emphasis on technological differentiation and real-world utility: solving actual problems, enabling genuine financial inclusion, and delivering on blockchain's theoretical advantages. This path promised purpose but required overcoming the sector's demonstrated preference for speculation over utility.

Most likely, cryptocurrency would continue straddling both paths, progressing on infrastructure and regulation while remaining fundamentally speculative. The question for 2026 and beyond wasn't whether crypto would survive - the infrastructure and capital commitment virtually ensured that. The question was whether it would evolve from a speculative asset class prone to massive volatility and security failures into something approaching its advocates' ambitious vision.

For now, 2025 stood as a stark reminder that technology alone couldn't overcome human nature's susceptibility to greed, fear, and operational error. It demonstrated that regulatory approval and institutional adoption, while necessary, weren't sufficient for sustained success. And it proved that in markets driven primarily by narrative and momentum rather than fundamentals and cash flows, even record-breaking peaks could precede devastating crashes.

The survivors of 2025's turbulence - whether individual investors, institutional allocators, or crypto companies - would carry these lessons forward, hopefully building more resilient systems, more realistic expectations, and more sustainable business models. Whether they would succeed remained an open question, but 2025 had certainly clarified the challenges ahead.